| 2002 |

|

YEAR BOOK |

CENTRAL STATISTICS OFFICE

|

Automatically filtering structural breaks in

economic indicators

|

|

|

In the Central Statistics Office (CSO) many short-term economic indicators can have sudden irregularities, known as structural breaks, that can severely distort the identification of underlying trends and growth rates. In some cases, filtering an economic indicator to detect and adjust for a structural break can greatly improve short-term analysis. The approach adopted is based on state-of-the-art developments in automatic linear Autoregressive Integrated Moving Average (ARIMA) time series modelling. In contrast, traditional ARIMA modelling requires expert manual intervention and analysis.

The first step in filtering an economic indicator involves automatically removing the effects of short-term fluctuations that increase in amplitude over time. Filtering then proceeds to detect and remove first and second order changes in the long-term movement of the economic indicator. This step ensures the resulting economic indicator is stationary.

The second filtering step automatically estimates a multi-plicative seasonal ARIMA model. Using an appropriate fixed regular, that is non-seasonal part-model, the remaining seasonal part of the ARIMA model is estimated. Then, with the seasonal part fixed, the regular part of the ARIMA model is estimated. Finally, the regular part is again fixed and the seasonal part of the ARIMA model re-estimated. This process generates a sequence of multiplicative seasonal ARIMA models. The model with the smallest Bayesian-Information-Criterion (BIC) is chosen as the one that is the �best� representation of the economic indicator.

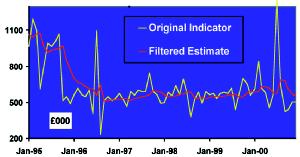

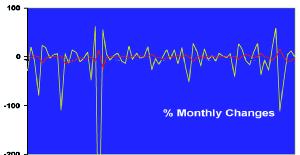

The final filtering step detects and adjusts for structural breaks in the economic indicator. Using the estimated seasonal ARIMA model, this step conducts a sequence of regressions based around an intervention analysis model. The intervention analysis model allows for four alternative transfer function forms representing four alternative types of structural break. When a structural break is found, it is incorporated into the intervention analysis model and the sequence of regressions repeated until no further structural breaks are detected. The accompanying Figure shows (i) the Original Indicator and the Filtered Estimate and (ii) the corresponding monthly changes.

Contact: [email protected]